Double, Double, Coil and Trouble: The Big Tech Pivot and Coiling Bond Yields

The Pioneer Perspective - Week Ending January 23, 2026

What We’ll Cover:

· Big Tech Growth Stocks Change Business Model

· The Bond Market and What Its Telling Us

· Historical Precedent

Big Tech and the Pivot From Growth to Efficiency

After historic gains in 2023/2024, some major players in the tech space are beginning to change their business model, albeit slightly. After years of having a tunnel-visioned growth mindset, many big names are now moving towards efficiency, infrastructure, and perhaps dividend increases. Let’s talk about three of the most recognizable names in the market and their shifting models.

1. NVDA 0.47%↑: In January, 2023 Nvidia was trading around $15 per share. As of January, 2026 Nvidia is trading in the $190 range. That’s a gain of 1,667% in just three years, absolute insanity. The chip titan has hinted they are moving from “growth at all costs” to keeping profit margins sustainable. Though projected to reach their revenue goal of $213 Billion this year, the question will no longer be about how many chips Nvidia can make, but rather how high they can keep their margins. The chip/AI market is becoming increasingly saturated with companies like AMD 2.59%↑, INTC 1.66%↑, and AMZN 2.51%↑ all stepping up their chip production. To navigate these crowded waters Nvidia is trending towards an infrastructure approach. Rather than just selling chips, it will be building data centers, working on autonomous vehicle integration, and robotics. Nvidia is expanding into broader fields because sustainability as a chip manufacturer without diversification is a potentially concerning business model. They have moved from hyper-growth to medium-growth with these recent moves. Because of this trend, we are likely to see more share buybacks and possibly even increased dividends down the line.

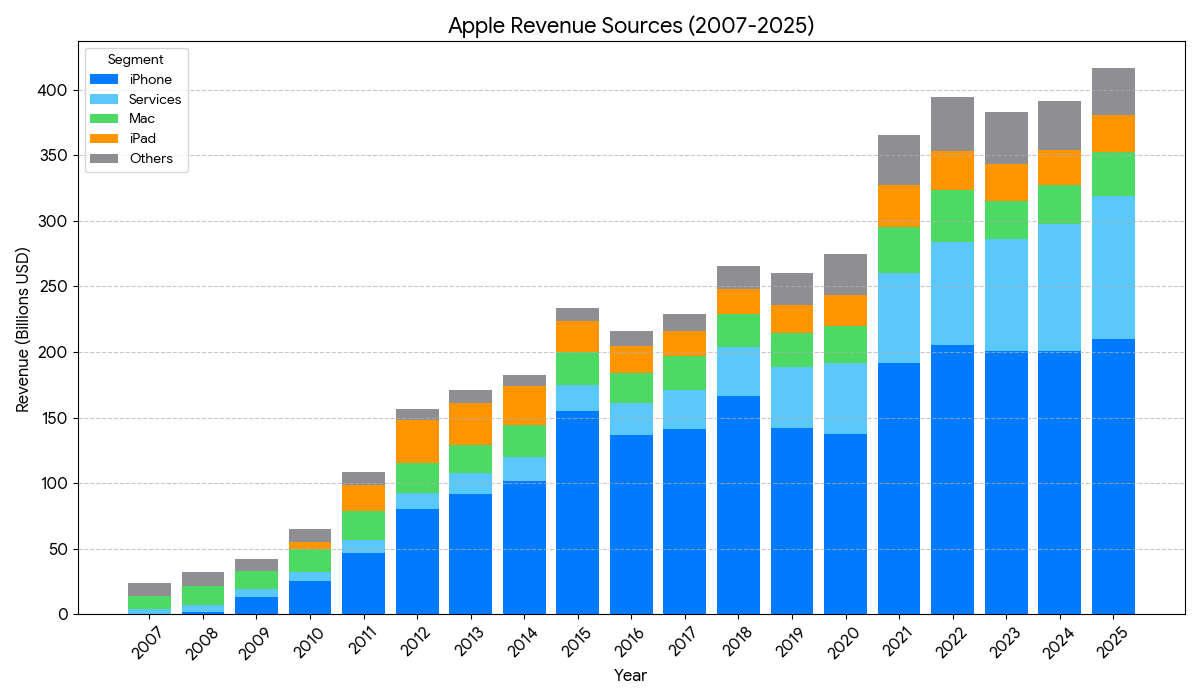

2. AAPL -1.62%↓: Apple is off to an undeniably slow year. The company’s stock price has tumbled 8.76% so far in 2026, and they have yet to see any meaningful bounce or trend reversal. Part of this is due to a slowdown in sales from their golden goose, the iPhone. The chart below is a notable representation of a potential business model change for Apple.

The important thing to note about this chart is not that the company is still growing, which it is, but the factors contributing to that growth. For example, in 2007 the iPhone accounted for just 1% of Apple’s revenue. By 2015 the iPhone accounted for a massive 67%. In 2025 however, we are seeing a change. While the iPhone is still the lead driver for them, it is decreasing as a percentage of overall revenue. iPhone sales have largely flattened over the last five years. Investors largely believe this is due to the lack of innovation. People are holding onto their iPhones longer because perhaps they don’t see a worthwhile difference between the iPhone 13 to the iPhone 16, etc. The growing source of revenue for Apple has become business services, which exceeded $200 Billion in revenue for 2025. This includes things like the iCloud, App Store, and now Apple Intelligence subscriptions. With this growth change we will also likely see a change in dividends. Although not announced until May, Apple is expected to increase its dividend payments by 4-7%. We don’t think the iPhone is going anywhere, but Apple is showing that they are adapting from a phone company to a business services company.

3. MSFT 0.93%↑: Yet another big tech name whose off to a volatile start this year. YTD Microsoft is down 3.65% and investors are worried the hyper-growth business model, which worked great up until now, may not be the most profitable option in the latter half of the 2020s. For example, Microsoft invested HEAVILY into OpenAI (ChatGPT) as a way to prove they are big competition in the AI gold rush. Yet, much to their misfortune, their OpenAI investment ended up costing roughly $3.1 Billion from their potential revenue last quarter alone, with little to show for it. The market sentiment has shifted from AI bullish speculation and is now forcing companies to show how revenue can actually be sustained. Gone are the days of simply saying the word “AI” during an earnings call 50+ times and watching your stock price surge 15% overnight. Revenue from Xbox sales have dropped, as well as Azure. Microsoft has made a huge AI bet and right now is having a hard time showing investors that this play is worthwhile. Microsoft reports earnings on Wednesday, January 28, and we will see if they talk about shifting business models from pure growth to service/infrastructure.

Bonds: Another Piece of the Puzzle

Bond prices, across the board, have been in a tight range for the better part of two years. The US10Y has been hovering between 3.6%-4.6% since December 2023. The US20Y and US30Y trading between 4.1%-5.1% for the same time period. After hitting their respective peaks in October 2023 they have been in a notably tight range. In the bond world, this tight trading is known as “Rangebound Consolidation” or “The Coil” and it usually signifies instability, despite having stable price action. This price movement means there is a tug-of-war in bonds and markets are unsure where the future is headed. What is the tug-of-war about this time? Recession vs. inflation.

· The Ceiling (Growth/Inflation): Every time yields try to break higher, the “manufacturing slowdown” narrative or unemployment data kicks in. Investors see the cooling economy and buy bonds (driving yields back down) because they expect a recession.

· The Floor (Tariffs/Debt): Every time yields try to break lower, “inflation fears” or “tariff threats” kick in. Investors realize that 100% tariffs on Canada or massive deficit spending will keep prices high, so they sell bonds (driving yields back up) because they don’t want to be stuck with low-yield debt in a high-inflation world. This coil can only go on for so long. Eventually, history tells us that it will SNAP in one direction or the other. The last example of elevated bond yields staying in a tight range for multiple years was under former Fed Chair Alan Greenspan. The US20Y traded between 4.2%-5.3% for four years, culminating in the 2008 financial crisis. Yields tanked and bond prices surged as investors fled to the safety of government-backed interest payments.

So, are we on the verge of a change in the business cycle? We’ve seen inflation cooling, unemployment rising, manufacturing cooling, commodities prices soaring, big tech stock prices stagnating, and bond prices in a tight coil. Only time can resolve this key conundrum. The classic 60/40 portfolio was made for uncertainty, and could be a viable option for these choppy waters. We believe we are indeed witnessing a business cycle transition. The issue is it’s impossible to predict how long the transition will last. Because of this uncertainty, we remain defensive in our portfolio with our largest positions being bond ETFs. Despite our defensive posturing we are still beating the S&P 500 by 2.28% YTD.

Want to know which investments we own? Subscribe to our Gold Members subscription. If you have a total portfolio value of $2,193 then the extra gains we’ve had the last three weeks will cover our monthly charge, meaning any portfolio value greater than this number is pure alpha. Try it for FREE for the first 90 days!

Pioneer Financial Gold Membership

Thanks for reading! Until next time, good luck out there and Godspeed.

© 2025 Pioneer Financial, LLC — All rights reserved. This newsletter is for informational and educational purposes only and does not constitute investment advice.