Nine Rings for Mortal Men: SCOTUS Decision, GDP, and Inflation

The Pioneer Perspective - Week Ending February 20, 2026

What We’ll Cover

· The SCOTUS decision regarding tariffs

· GDP: Is it as bad as the headline number?

· Inflation and the Fed’s next move

· Summary

Supreme Court Decision

“And nine, nine rings were gifted to the race of Men, who above all else desire power. For within these rings was bound the strength and the will to govern each race. But they were all of them deceived, for another ring was made. Deep in the land of Mordor, in the Fires of Mount Doom, the Dark Lord Sauron forged a master ring, and into this ring he poured his cruelty, his malice and his will to dominate all life.

One ring to rule them all.”

On Friday, in a 6-3 decision, the supreme court struck down President Trump’s tariff policy. Specifically, they stated that President Trump exceeded his authority under the International Emergency Economic Powers Act (IEEPA) of 1977. The IEEPA is what POTUS used to bypass congressional approval and start enacting broad-ranging tariffs across the globe. The 1977 Act gives the president sweeping authority to make decisions under the precedent that the nation is under an emergency. To fulfill this requirement, President Trump claimed that the surge of fentanyl over the last decade constitutes a national emergency, and that tariffs are a way to lever action against rising drug overdoses. Chief Justice Roberts wrote the majority opinion for the court. Here is a key statement from his opinion:

“The president asserts the extraordinary power to unilaterally impose tariffs of unlimited amount, duration, and scope. In light of the breadth, history, and constitutional context of that asserted authority, he must identify clear congressional authorization to exercise it.”

The highest court in the land is not suggesting that President Trump cannot use his power to enact tariffs, they are saying he can’t just do them whenever he wants for whatever reason for whatever length of time. They claim the authority for broad sweeping tariffs, exempting times of national emergency, remains with congress. In light of this, not all of the President’s tariffs were struck down. For example, tariffs. enacted under the umbrella of other laws are still in effect, specifically ones against China. That didn’t stop the President from making some spicy remarks against the Justices, especially those that he personally appointed. We don’t need to get into exact quotes, but let’s just say he sees it as a direct betrayal from those who ruled against him, despite appointing them to a position which demands an unapologetically a-political frame of mind.

Control of tariffs, a power so seductive that every President wants to wield it, but it eventually corrupts the balance of power. The Supreme Court just tried to cast that power back into the fires of Mount Doom, or in this case the halls of Congress, where it was originally forged.

What’s more, President Trump has already retaliated with new policy moves, targeting ways to legally work around this crippling ruling. He signed a proclamation using Section 122 of the Trade Act of 1974. This law allows the President to impose temporary surcharges of up to 15% for 150 days to deal with “large and serious balance-of-payments deficits.” While the 150-day limit sounds like a win for free-traders, the administration has hinted they could simply renew the declaration every five months, essentially creating a perpetual temporary tariff. This new 10% global tariff is set to kick in this Tuesday, February 24, 2026.

Markets reacted positively to the supreme court ruling, viewing the tariff halt as an immediate tax cut for investors. The major indices rose on hopes that prices would drop and the extra cash would help stimulate the economy and the stock market. The tariff ruling also stated that the money accumulated from the policy may have to be returned, causing companies to clammer at the idea that up to $200 billion may be placed back in their pockets.

Gross Domestic Product

The supreme court ruling wasn’t the only big surprise this week. GDP numbers came in far below estimates. The headline number came in at 1.4% annual growth for the fourth quarter of 2025, well below the consensus forecast of 2.8% and a sharp drop from the blistering 4.4% we saw in Q3.

Before you panic, or salivate in the case of our bears out there, this was almost certainly due to the extended government shutdown at the end of 2025. The Bureau of Economic Analysis (BEA) claims that the shutdown of federal services alone was responsible for a loss of 1.0% of the overall number. During Q4, 2025 federal spending plummeted as much as 16% on an annualized basis. This means that not only were federal employees not going to work, but spending was largely halted to all companies that depend on federal contracts.

Consumer spending slowed as well to 2.4% from 2.9%, annualized. The data showed that consumers are still spending on necessities and services (healthcare, insurance, etc.) but discretionary spending on physical goods declined rather sharply. High-income earners are the primary engine that is still driving this economy, as blue collar workers are starting to show signs of exhaustion. In contrast to consumer spending, business investing saw a nice annualized jump of 3.8%. This is once again fueled by AI investment and infrastructure. Investors are betting that the increased productivity to a largely AI workforce will offset the lack of job availability.

The Inflationary Plot Twist

So, we have massively declining GDP, albeit likely superficial, along with a tariff strike down, and unemployment slightly above average from the last few years. Well, as if on cue, PCE data came in and threw a right hook to the jaws of investors. Core PCE came in at 3.0%, up from 2.9% YoY This upside surprise was a reality check for markets, showing that inflation may be even stickier than they had expected.

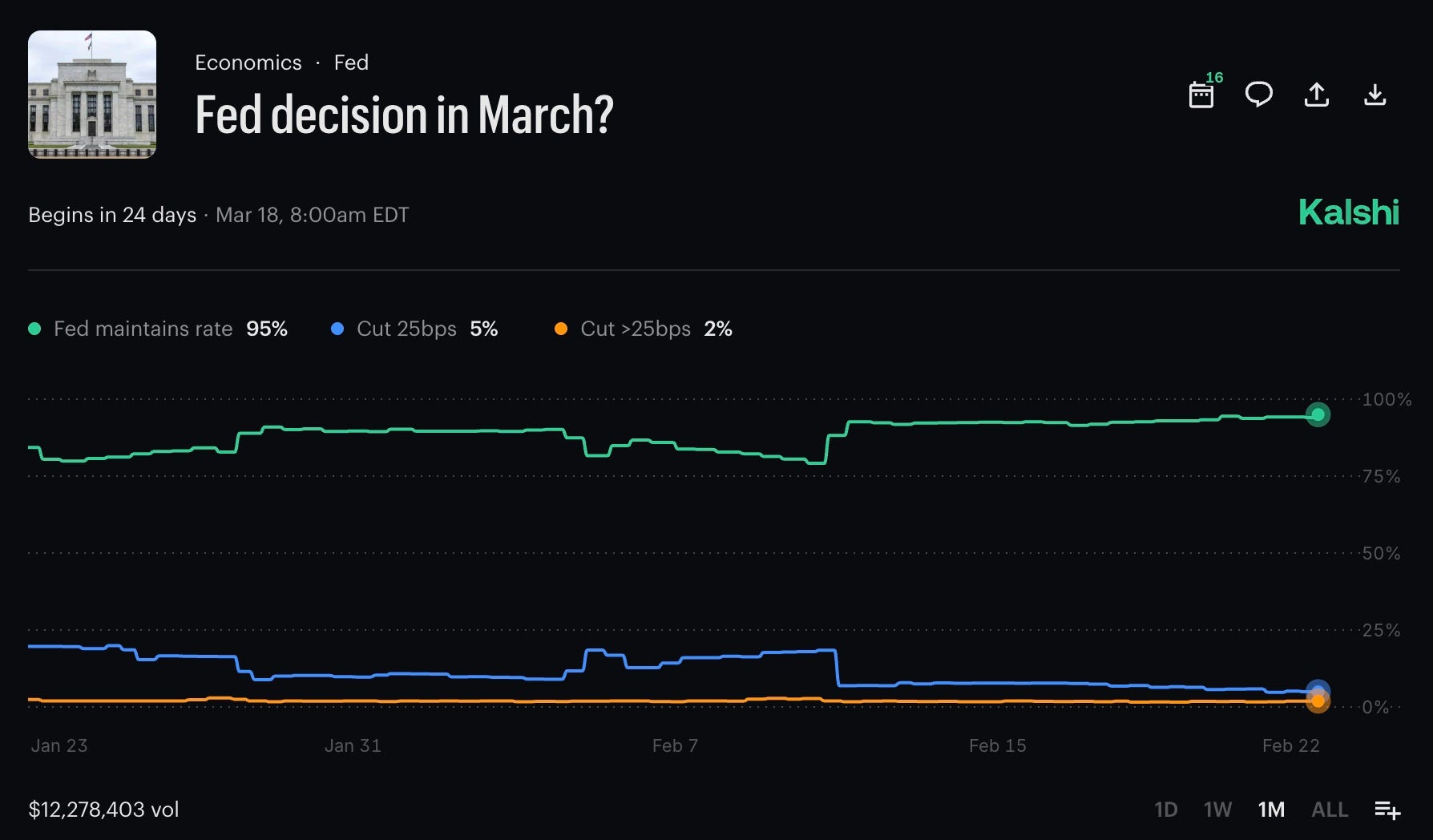

The Federal Reserve is now in a tough spot, per the usual arrangement, as they now have to weigh a clearly slowing economy with sticky inflation. Under normal circumstances a 1.4% GDP print would almost certainly warrant a rate cut, but now the Fed’s hands are tied. “Higher for longer” narratives have already started flooding the headlines, with Kalshi betting markets now predicting a 95% chance the Fed will hold rates steady at the March meeting.

Retrieved from https://kalshi.com/markets/kxfeddecision/fed-meeting/kxfeddecision-26mar on 02/22/2026.

We’ve talked before about sticky inflation and the route causes, which are sectors that people always need, even during recessions. In the latest data, once again service inflation is the culprit. While goods prices (like cars and electronics) are flat or falling, service inflation (rent, healthcare, insurance) is still running at roughly 3.4%. This is much harder to break with just a few months of slow growth. Economists noticed that “Real Final Sales” (a measure of actual demand) grew at 2.4%, much faster than the 1.4% GDP headline. This suggests the underlying economy is still quite warm, giving the Fed even less reason to rush into a rate cut. It seems the case for a rate pause at the March meeting is all but certain.

Summary

This week delivered a rare economic triple-threat that has left investors and policymakers alike navigating a sudden shift in the financial landscape. At the center of the storm was the GDP advance estimate, which revealed that the U.S. economy hit a significant wall in late 2025, growing at a meager 1.4% annual rate in the fourth quarter. This soft print was largely the result of the 43-day federal government shutdown that paralyzed Washington through October and November, a disruption that economists estimate shaved at least a full percentage point off the headline growth figure. While the private sector showed some underlying resilience, specifically in AI-driven business investment, the overall deceleration from the 4.4% growth seen in the previous quarter suggests that the “economic engine” is currently cooling faster than many had anticipated.

Compounding this growth slowdown was a cold shower from the PCE inflation data, which arrived with an unwelcome upside surprise. The Federal Reserve’s preferred gauge, Core PCE, climbed to 3.0% year-over-year in December, while the monthly increase of 0.4% signaled that inflation remains stubbornly sticky despite the broader economic cooling. This combination has created a classic stagflationary headache for the Federal Reserve. While the weak GDP numbers might normally justify a rate cut to stimulate growth, the heat in the inflation data has effectively locked the Fed into a higher-for-longer stance. Consequently, market expectations for a March rate cut have almost entirely evaporated, with traders now bracing for a spring and summer of high borrowing costs as the Fed waits for prices to truly break.

Thanks for reading, until next time.

Good luck and Godspeed.

***Subscribe to become a Gold Member and get access to our real portfolio! To celebrate our launch we are offering a free 90 day trial for a limited time. Link below!***

© 2025 Pioneer Financial, LLC — All rights reserved. This newsletter is for informational and educational purposes only and does not constitute investment advice.