Why Your Credit Card Might Not Work After January 20, 2026

The Pioneer Perspective - Week Ending January 16, 2026

What We’ll Cover

· President Trump’s 10% Credit Card Interest Cap

· Geopolitical Tensions With Iranian Protests

· Inflation - Is it under control?

The 10% Proposed Cap For Credit Cards

On Friday, January 9, President Trump proposed a 10% limit on the interest payments that banks are allowed to charge on their credit cards. This isn’t just a hit to potential banking profits, but rather a complete restructuring of America’s lending system. The average interest on credit card debt is 21%, so a 10% cap is staggering. For example, if you owe $10,000 in debt then you are likely paying north of $175 PER MONTH in interest payments. The 10% cap would drop your payments to roughly $80, resulting in noticeable savings. For some families, this can save them years of payments because that newfound wealth of $120/month would now go towards the principle instead of the interest alone. This move by the President is obviously meant to cut costs for the average American, however there may be some sinister risks and changes to your wallet. Let’s talk about them.

1. The Credit Limit Slash: If you have a high amount of credit card debt, you now run the risk of banks simply slashing your credit limit. This is an issue for Americans that rely on credit cards to make ends meat. Most banks will base their models around 20%, which means that they have an increased risk of taking on defaults when interest rates are slashed to 10%. In practice, this might look something like having $10,000 in debt with a $15,000 credit limit. With the new 10% cap, banks may suddenly slash your limit to $10,000 which would have two primary consequences. First, you are now maxed on your credit limit which gives you no room for a rainy day. Second, it puts your credit usage at 99% which will tank your credit score by anywhere from 25-100 points based on your history. A perfect payment history won’t matter because your limit is now decreased.

2. The Account Freeze: If you have a credit score below 700 then please read carefully. Banks have already threatened to simply freeze accounts for sub-prime or near-prime borrowers to mitigate their risk. This means that if you have a credit limit of $10,000 with a credit score that isn’t “excellent” you may see your account frozen. You will still be able to pay off the debt you owe, but new transactions on the card may be frozen. We know this may be concerning for many readers, so please see the links below. This may have a significant impact on your finances.

3. The Fee Pivot: Since banks will be losing money from lower interest payments they will likely hunt for it in other places. Increasing fees is an easy workaround for them to enforce. For example, if your credit card has no annual fee then you may wake up and suddenly see a $100 charge to the card due to “changes in fee policy.” You might also see an increase in fees for late payments. Lastly, a way they can increase profit is to devalue points/miles. Maybe now you have $500 worth of points on your card, but that value may significantly decrease so the banks can save more money by taking away your rewards.

God Bless the First Amendment

Geopolitical tensions with Iran have been especially high of late. For the last 45 years the Iranian people have been under the rule of the Ayatollahs. In 1979, the leader of Iran (Shah) was overthrown in his attempts to turn Iran into a westernized nation. Religious fundamentalists took over and established the theocratic monarchy that we see today. In late December 2025 protests began erupting all over the country to demonstrate opposition to the current regime. Peaceful assembly is not a constitutional right in Iran as it is here in the US, so naturally we began to see violence. In an attempt to quash all protests Iranian soldiers escalated tensions by using lethal force against civilians en masse. Though it is difficult to get an exact calculation, the death toll estimates is in the range of 2,000 (according to Amnesty.org) all the way up to 20,000 (CBS News). After President Trump put pressure on the Ayatollahs, and after his proven willingness to strike the regime directly, tensions cooled. On January 15, President Trump noted that the regime has largely calmed down in their violent tactics of murdering civilians. There is another reason for this recent deescalation, and it comes in the form of the richest man in the world.

Enter Elon Musk. The Ayatollahs cut off all communications in Iran, preventing civilians from showing the world the true extent of the violence. Elon Musk had a meeting with President Trump, culminating in Musk giving free access to Starlink to anyone in Iran with a terminal. Shortly thereafter, the violence was being live streamed in front of the whole world. The attempts of the regime to keep the protests silent had ultimately failed. This move by Musk has demonstrated to investors that SpaceX has potential to be a major geopolitical asset in the future. This is why we are invested in space. In the future, the country that holds the power in space will ultimately be the dominant force in the world.

Inflation

CPI data was reported this week, coming in at 2.7% YoY. The primary driver of inflation is oil prices, which is in a strong downtrend. Despite the mid-week spike, we are witnessing prices dip back to their lows. As oil prices continue to drop the remaining driver of sticky inflation is housing. Rent and mortgages are still high, relatively speaking, and they are proving difficult to handle on a policy level. The average 30-year mortgage has dropped below 6.1% for the first time in three years, yet housing prices are still at all-time highs. So, while interest payments on the loans may be going down, many families still cannot afford to buy a house.

To mitigate the housing affordability crisis, President Trump has focused his attention on two targets: mortgage bonds and institutional ownership of homes. On January 8, Trump directed Fannie Mae and Freddie Mac to purchase $200 billion worth of mortgage-backed securities. The hope is that by increasing the demand for these bonds it will cause mortgage rates to fall. This is part of the reason we’ve seen a recent drop in the 30-year mortgage, though critics have suggested that this move has the potential to reignite inflation.

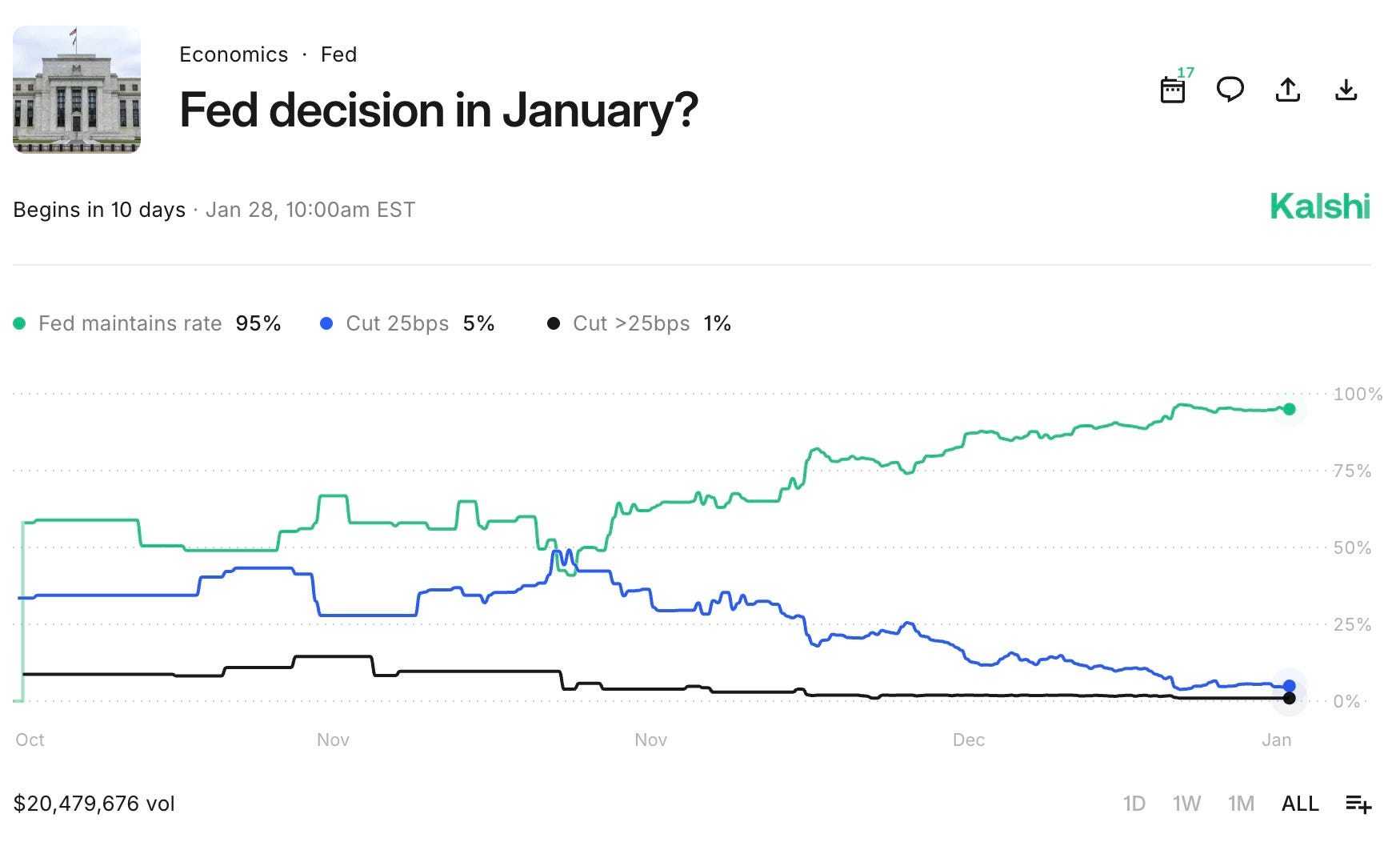

So how does institutional ownership come into play with family housing? The answer is Blackstone. On Truth Social, Trump announced his plans to ban institutional ownership of single-family homes. Companies like Blackstone have managed to hoard 5% of all single-family homes, often outbidding actual families with generous cash offers. If this proposal passes congress then we could see a major rotation of capital out of the real estate market and into other sectors, potentially equities. Only time will tell if these plans by President Trump will bare fruit. With the Federal Reserve being in a neutral-rate position, only a strong change in the labor market or inflation would encourage them to keep cutting rates. This tells us that investors see inflation as mostly under control, yet still sticky in certain sectors. As of now, Kalshi betting markets show a 95% chance that the Fed will HOLD interest rates at current levels.

Retrieved from https://kalshi.com/markets/kxfeddecision/fed-meeting/kxfeddecision-26jan on January 18, 2026.

So What?

Here’s how this impacts US markets. We saw a spike in WTI crude during the week due to fears of a blockade being placed in the Straights of Hormuz. For reference, 25% of global oil is traded through these waters. They provide access to virtually all Middle Eastern countries via the Persian Gulf. Iran, Qatar, UAE, Bahrain, and Kuwait all have stretches of shoreline in the Persian Gulf, which has made it a massive trading hub. WTI crude oil has recently dropped back to roughly $59/barrel now that the war premium has largely subsided. Gold has also seen some volatility. After surging to over $4,650/oz, it has declined back to a current price of $4,500. Despite heavy profit-taking, precious metal prices remain elevated.

We’re not here to tell you what we think of President Trump, whether you admire him or strongly dislike him is for each to decide on their own. However, what we can all agree on is that the man is volatile. Part of his process for initiating policy is to be unpredictable. Because of this, we have no clue what idea or proposal he will come up with each week. We believe it is best practice, especially right now with so many red flags in the market, to be well diversified and defensive with our portfolio. This is not the time to buy everything, nor is it the time to sell everything. It’s the time to be pragmatic in thoughtful into every single securities trade. We remain bullish on bond ETFs, as well as the S&P 500. Many of the recent headlines have already been priced into the market as we look forward into next week. Be careful of not over-leveraging into one position, or even one sector. You never know when a top secret military strike could take place at 2:00 in the morning and flip the western hemisphere on its head, as we saw just a few short weeks ago.

If you want to see exactly how our assets are allocated then subscribe to our Gold Membership! Try it for FREE for the first 90 days!

Pioneer Financial Gold Membership

Thanks for reading! Until next time, good luck out there and Godspeed.

© 2025 Pioneer Financial, LLC — All rights reserved. This newsletter is for informational and educational purposes only and does not constitute investment advice.